How are City budgets different than private sector budgets?

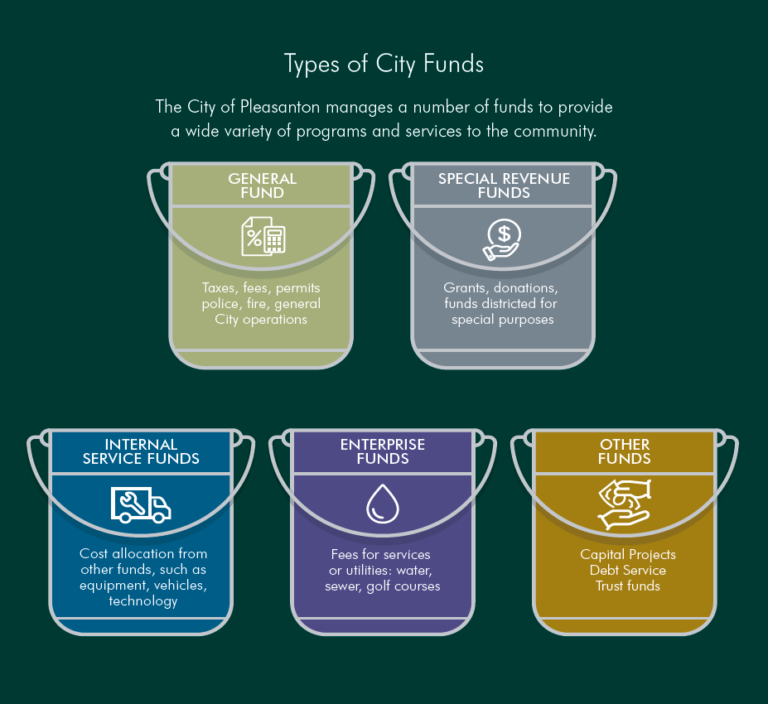

What are the different categories of public funds and how can they be used?

What is the General Fund?

What is a special fund?

What is the difference between the general fund and enterprise funds?

What is the difference between “one-time” and “ongoing” funding?

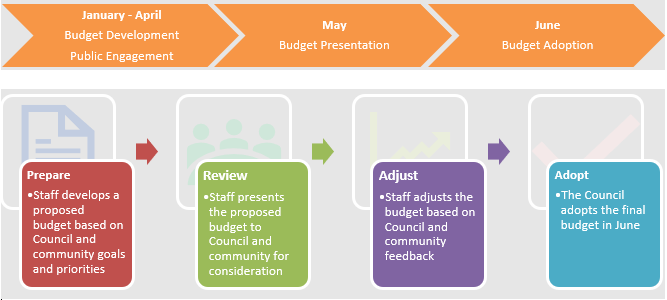

What is the Operating Budget?

What is the Capital Budget?

When is the City’s fiscal year?

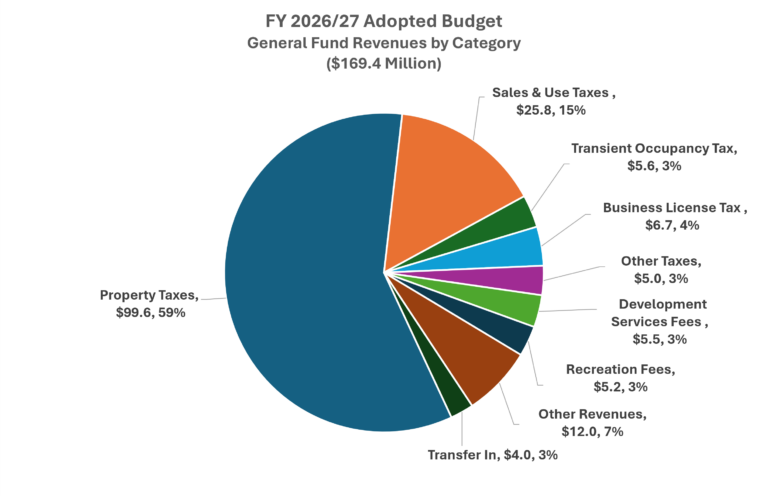

What is the largest revenue (income) source in the City’s General Fund?

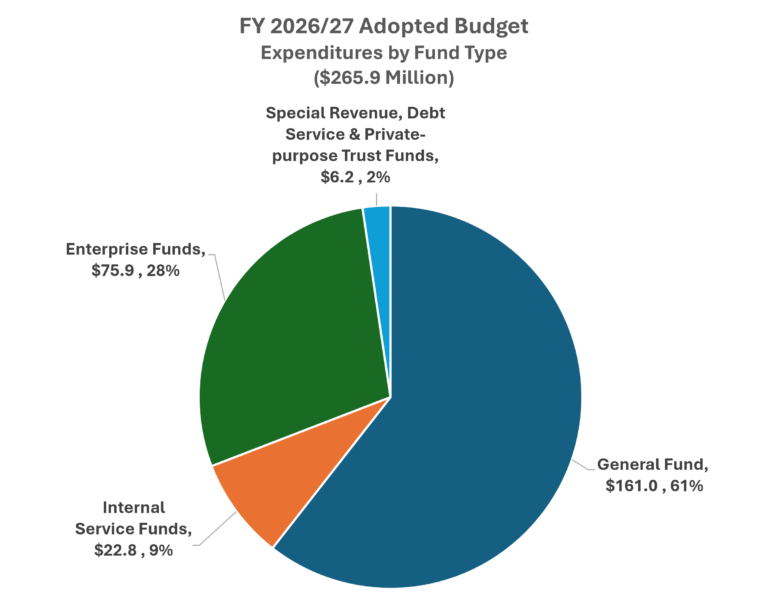

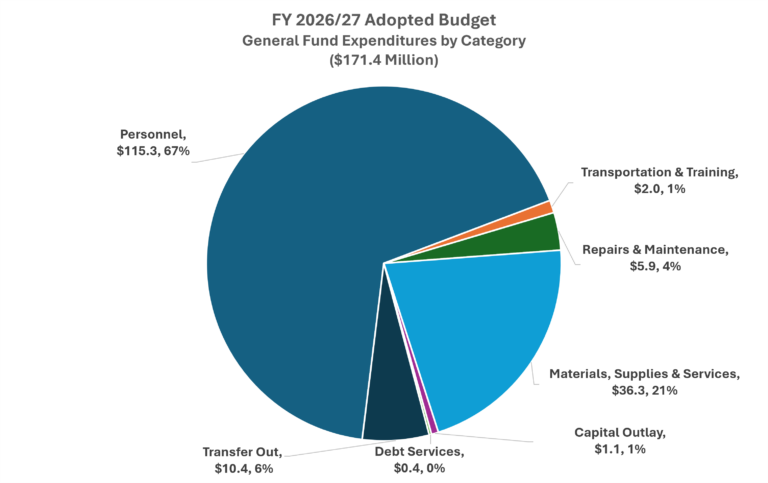

What is the biggest expenditure (expense) in the City’s General Fund?

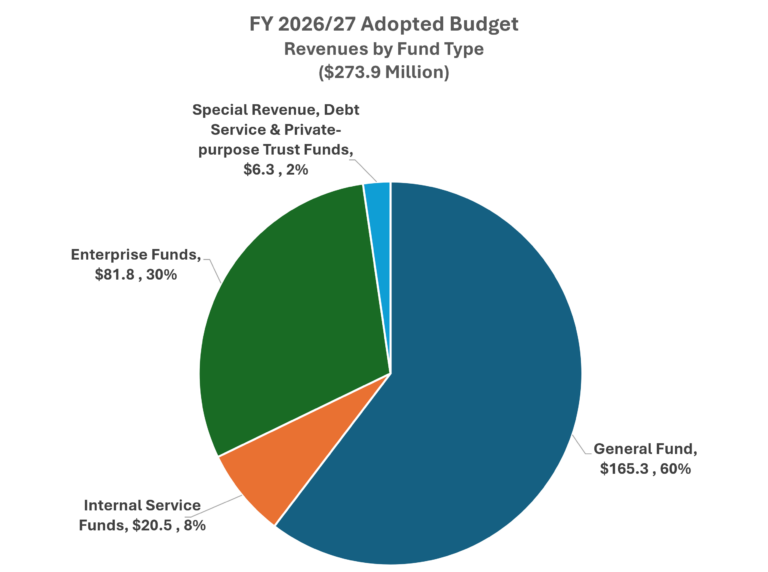

Where do City funds come from?

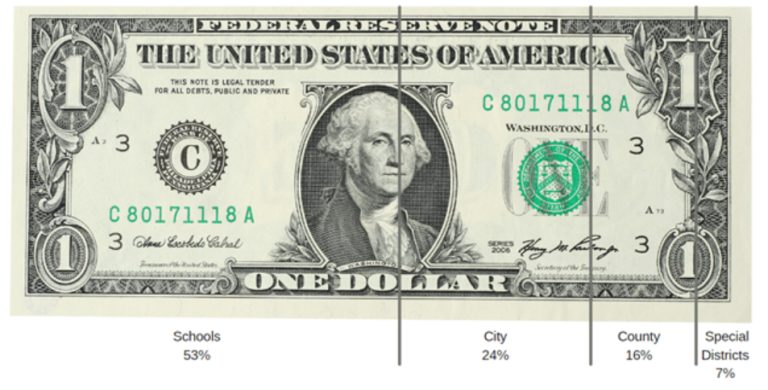

Where does your property tax dollar go?

What are the City's sales tax revenues by category?

What do City funds pay for?